This blog reveals what a massive 37,804 AI respons...

This blog explores how the IT industry is being re...

This blog explains how IcyPluto uses link intent—a...

India's life insurance market has crossed a defining threshold. With new business premiums reaching ₹3,48,424 crore between April 2025 and January 2026 — a 14% year-on-year jump — the sector has moved well past its post-pandemic consolidation phase and into a period of sustained, broad-based expansion. According to TechSci Research, the Indian life insurance market was valued at USD 140.47 billion in 2025 and is projected to nearly double to USD 261.53 billion by 2031, growing at a CAGR of 10.97%.

But beyond the premium numbers lies a far more nuanced competitive story — one that is now being shaped, in real time, by artificial intelligence.

At IcyPluto, we built our entire operating philosophy around one idea: that in an AI-first world, a brand's presence in generative AI conversations is just as valuable, if not more so, than its presence on a traditional search engine results page. That's why we used our proprietary AI intelligence infrastructure to run over 1,000 structured prompts across five leading large language model platforms — ChatGPT, Claude, Perplexity, Copilot, and Gemini — to map exactly which insurance brands are dominating the AI-driven mindshare of Indian consumers and investors.

The result is this report: a deep, data-backed competitive analysis of India's top 10 life insurance providers, anchored in both conventional market metrics and next-generation AI brand visibility signals. If you are a brand strategist, investor, policy researcher, or a senior marketer trying to understand where the Indian insurance space is heading — this is the most comprehensive picture available right now.

Before getting into individual brand performance, it is important to understand the ground on which these companies are competing. India's life insurance sector is not just large it is structurally transforming.

A Market Growing Faster Than the Economy

India's life insurance industry logged its strongest single-month growth in nearly two years in December 2025, with new business premiums rising 39.5% year-on-year to USD 4.6 billion (₹421.5 billion), according to CareEdge Ratings. That was the fourth consecutive month of double-digit growth, following a brief contraction in August 2025. The recovery has been driven by a combination of product-level demand surge, the government's GST waiver on individual life insurance premiums, and the wider rollout of initiatives under the BIMA Trinity framework — including Bima Sugam, a digital insurance marketplace that is reshaping how policies are distributed and serviced.

Swiss Re, in its January 2026 market outlook, forecast India's insurance market to grow at 6.9% annually in real terms from 2026 to 2030, outpacing most major emerging economies. For context, that positions India among the top three fastest-growing large insurance markets in the world, alongside Indonesia and Vietnam.

The Regulatory Environment Is Actively Reshaping Competition

The Insurance Regulatory and Development Authority of India (IRDAI) has been progressively liberal in its approach over the past two years. The GST relief on individual life policies removed one of the key friction points that had been suppressing uptake among middle-income households. Meanwhile, digital-first distribution models have given private insurers meaningful avenues to reach demographics that were traditionally underserved by LIC's branch-heavy infrastructure.

In FY 2024–25, the entire insurance sector issued 41.84 crore policies, collected premiums worth ₹11.93 lakh crore, and paid out claims totalling ₹8.36 lakh crore. These are not small numbers. They reflect an industry that has matured into a critical pillar of India's financial services ecosystem.

The Annual Premium Equivalent (APE) for the industry rose 28.3% year-on-year in December 2025 alone, led by a 44.1% increase at LIC and a 22.8% rise across private insurers. Within the private segment, Axis Max Life posted 20% APE growth over the April–January FY26 period, signalling that the mid-tier challengers are closing ground on the market leaders faster than many analysts anticipated.

IcyPluto's core product suite is built around Generative Engine Optimization — or GEO. Unlike traditional SEO, which tracks a brand's rank on a Google results page, GEO tracks whether and how a brand appears in the responses generated by large language models when a user asks a conversational question.

The Methodology: 10,000+ Prompts, Five Platforms

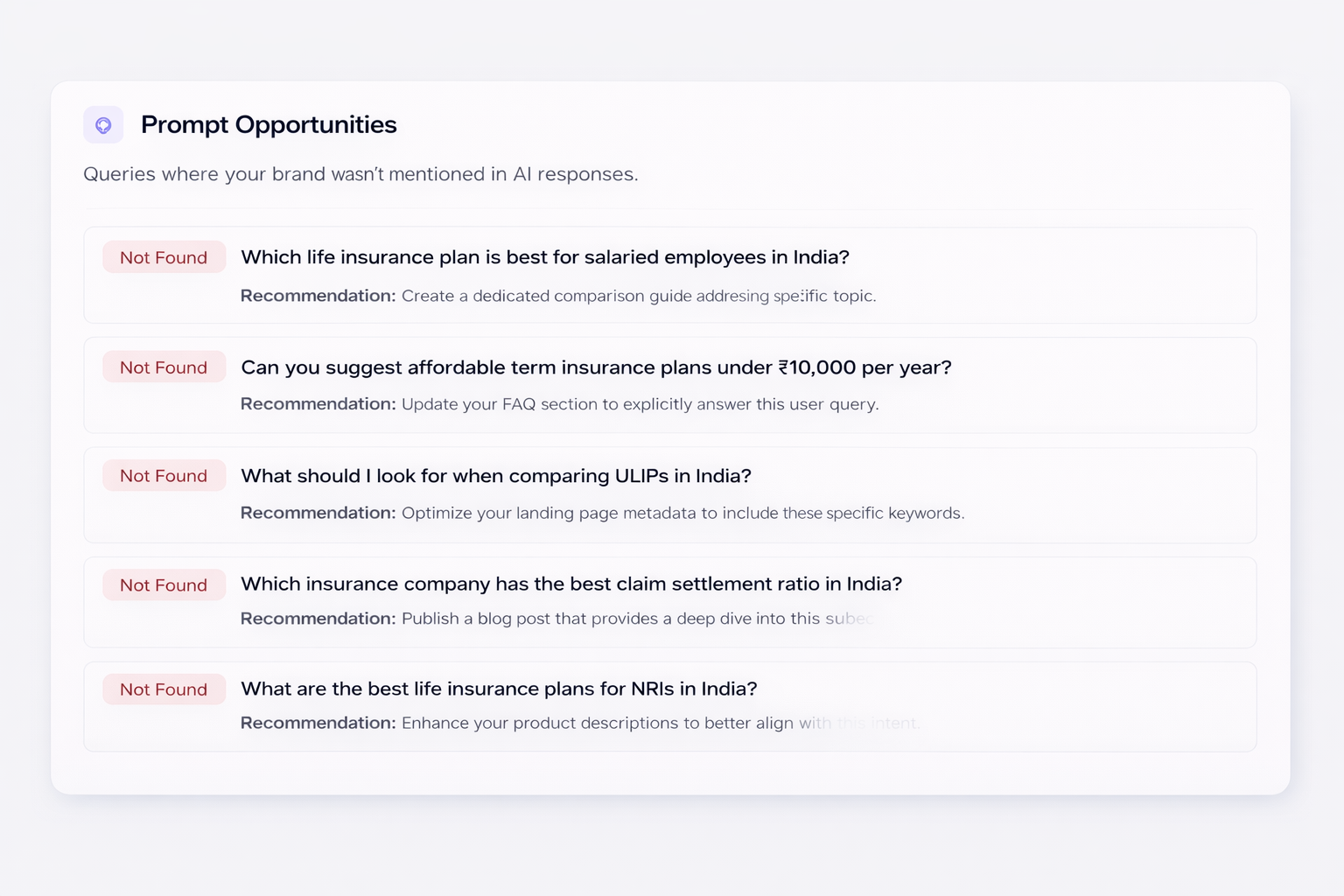

Our AI intelligence team ran over 10,000 structured prompts across ChatGPT, Claude, Perplexity, Microsoft Copilot, and Google Gemini. The prompts spanned multiple categories: general consumer queries (e.g., "Which insurance company should I choose in India?"), research-oriented questions (e.g., "What are the top life insurance companies in India by market share?"), comparison queries (e.g., "LIC vs HDFC Life — which is better?"), and trust-signal questions (e.g., "Which insurance company has the best claim settlement ratio in India?").

Across these 10,000+ prompts, we tracked frequency of mention, position within AI responses (whether a brand appeared first, second, or third), consistency across platforms, and qualitative sentiment signals — whether the brand was described in positive, neutral, or cautionary terms.

This is not a traditional survey. There were no human respondents. What we measured is the embedded intelligence of five of the world's most widely used AI systems — a reflection of the aggregated data, news coverage, consumer opinion, and expert analysis these models have been trained on. In that sense, AI brand visibility is arguably the most unfiltered proxy for a brand's real-world reputation that exists today.

What the Data Revealed

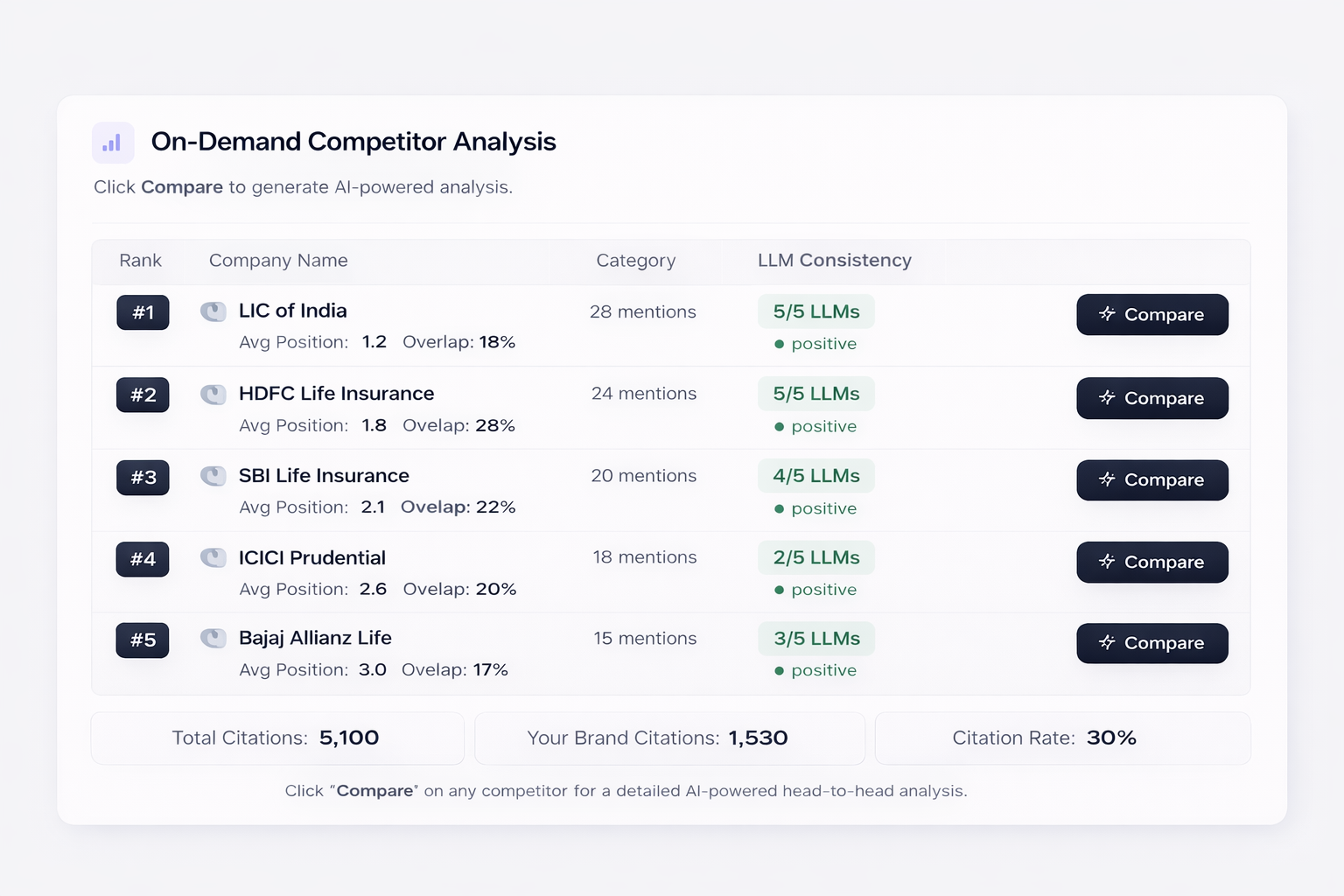

Ten companies consistently appeared across all five LLMs when users queried India's insurance sector. These ten brands dominated AI-generated responses regardless of how the question was framed whether the user asked about market leaders, trusted brands, or recommended policies. That consistency itself is a powerful signal: these are the companies that own the insurance narrative in India's AI-driven information ecosystem.

The ten companies, identified through IcyPluto's 10,000+ prompt analysis, are:

Life Insurance Corporation of India (LIC)

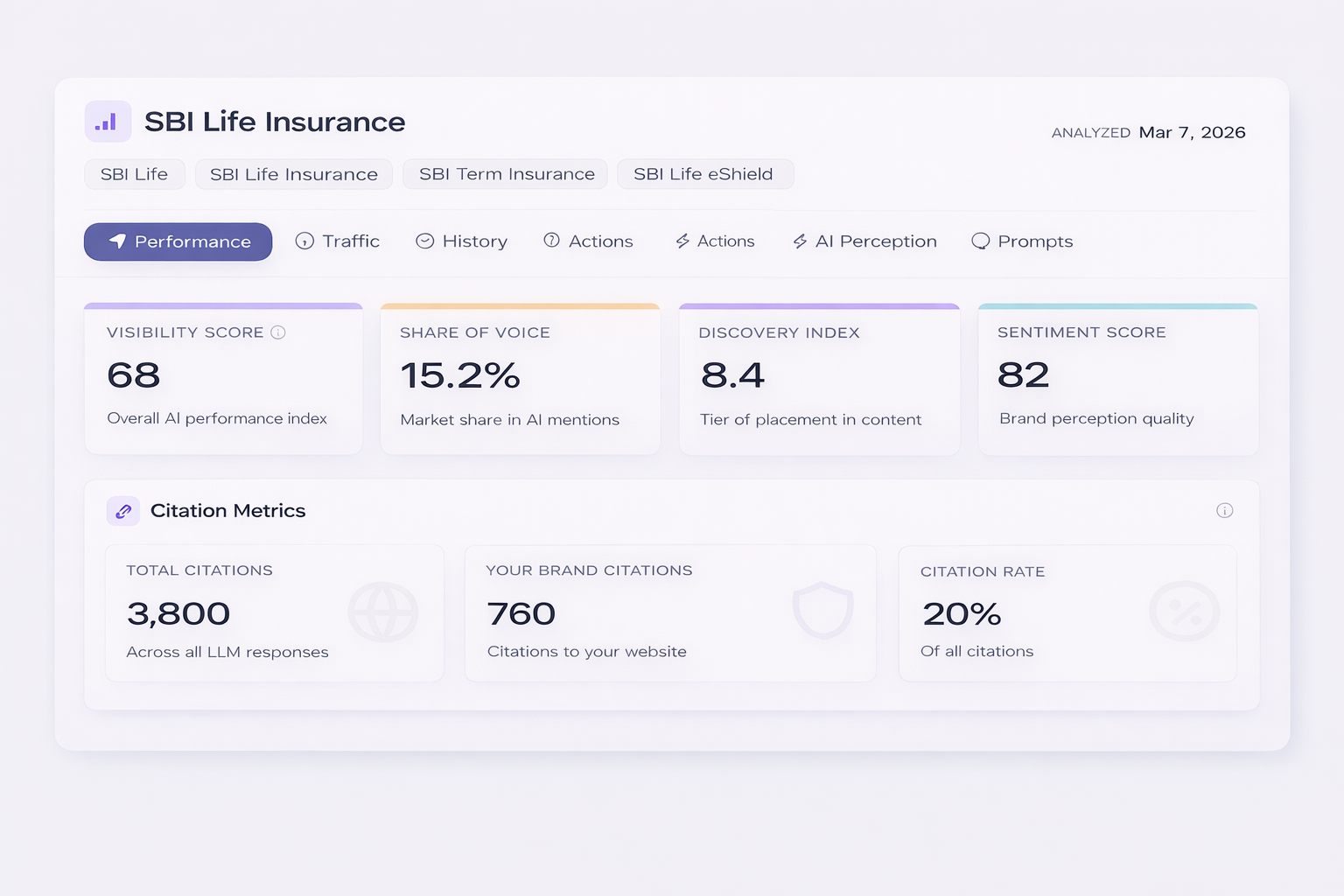

SBI Life Insurance

HDFC Life Insurance

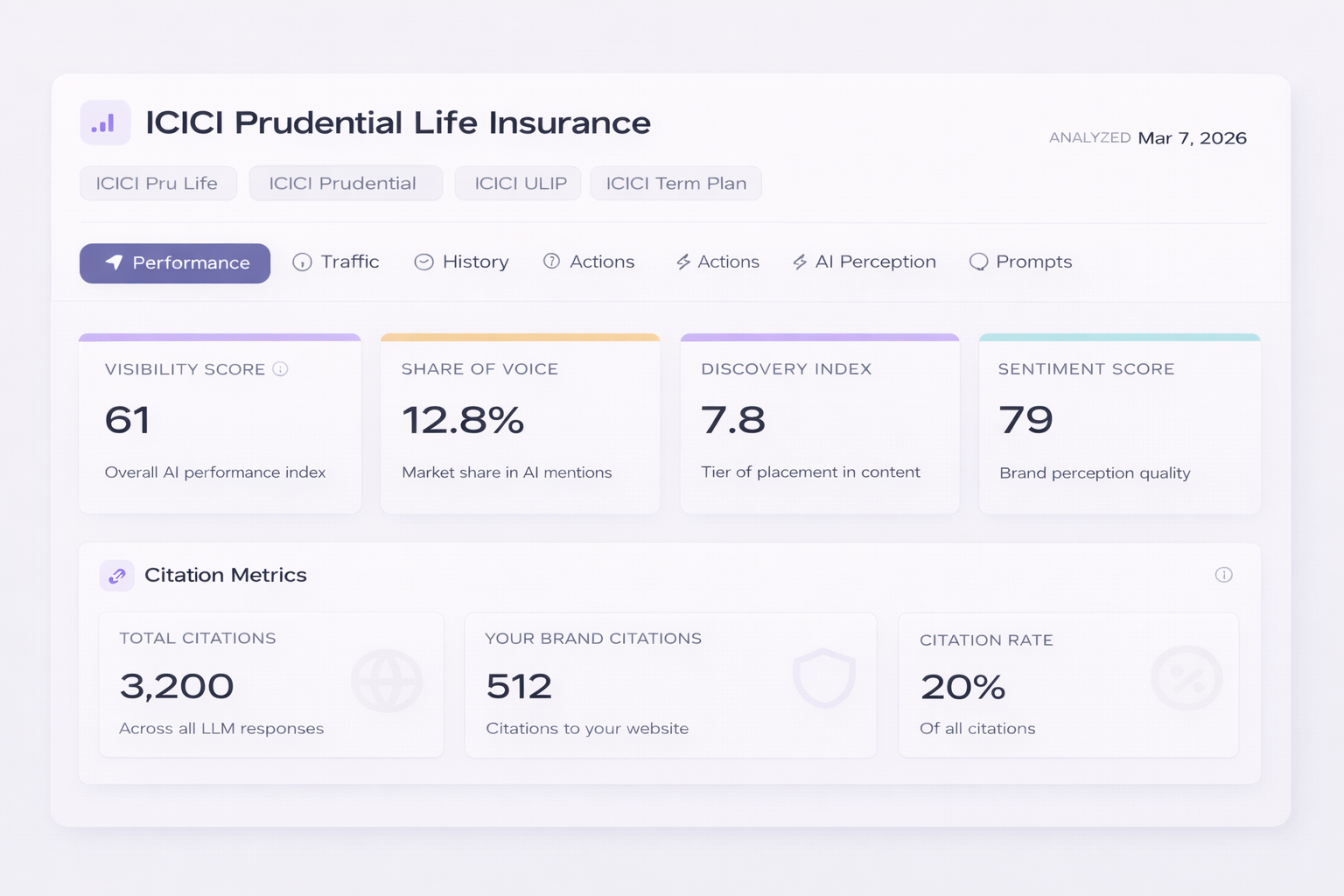

ICICI Prudential Life Insurance

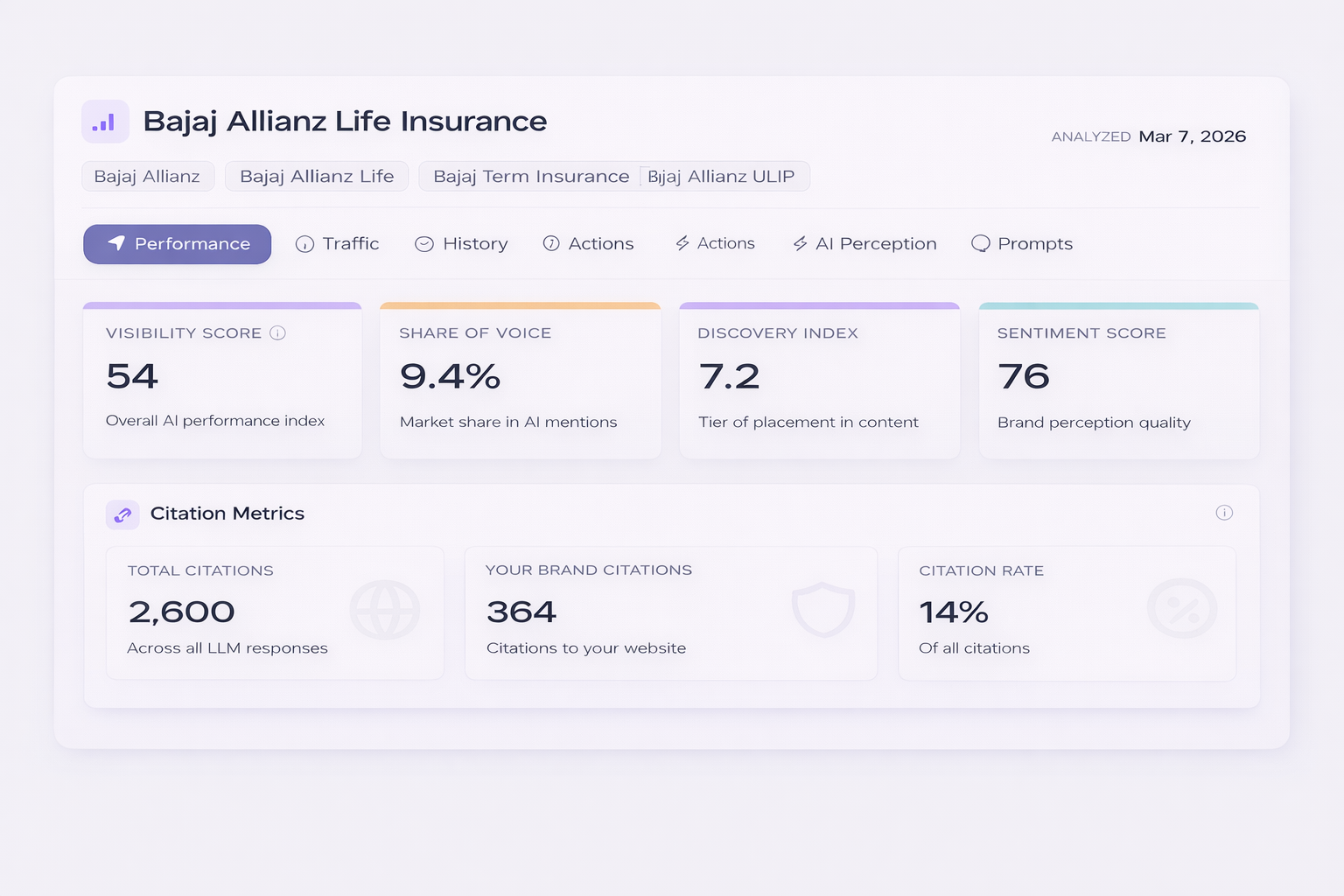

Bajaj Allianz Life Insurance

Tata AIA Life Insurance

Kotak Mahindra Life Insurance

Aditya Birla Sun Life Insurance

Max Life Insurance (now Axis Max Life Insurance)

PNB MetLife India Insurance

What follows is a company-by-company breakdown. Each profile combines conventional market data — premiums, market share, claim ratios with insights derived from IcyPluto's AI visibility research.

1. Life Insurance Corporation of India (LIC)

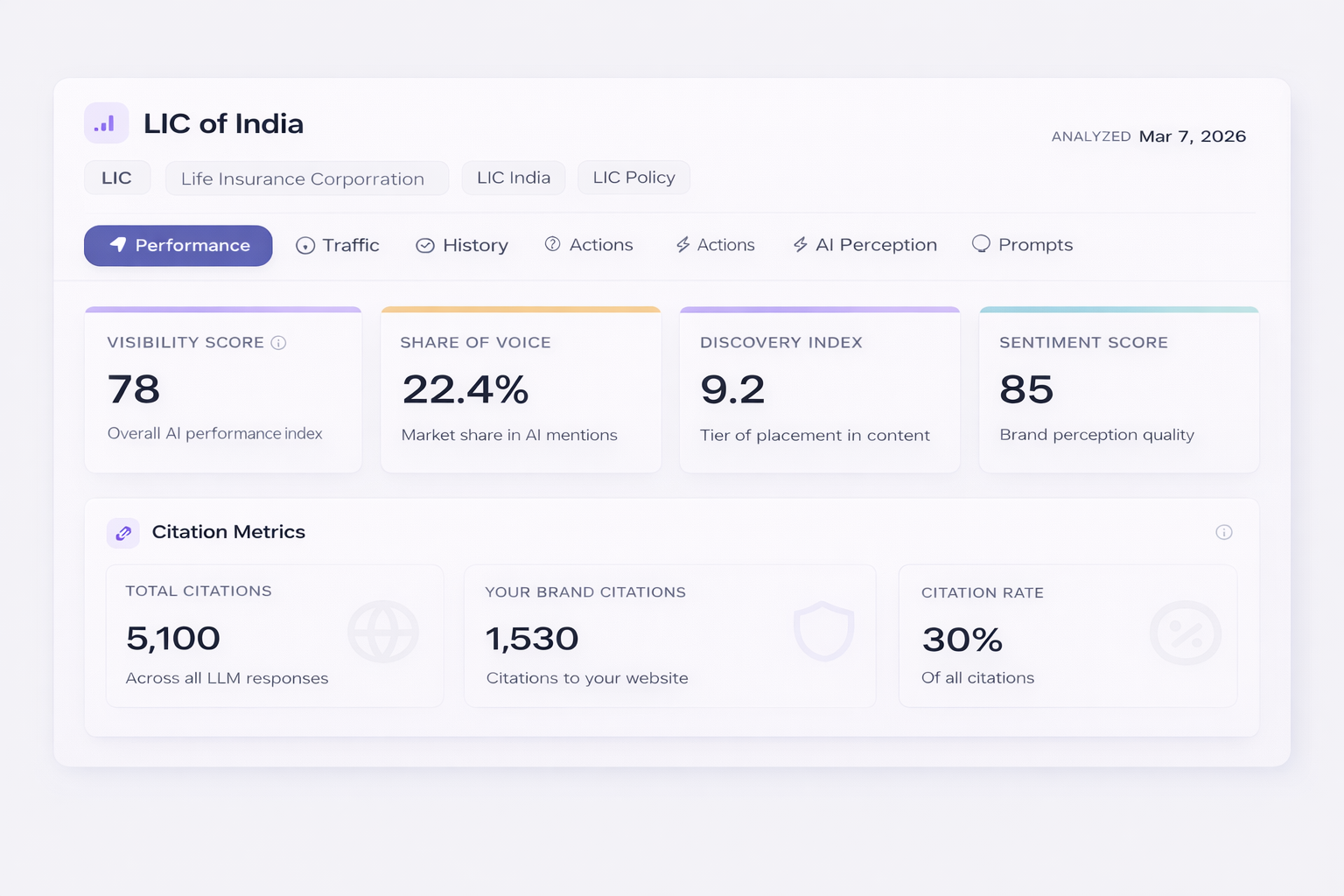

There is no equivalent to LIC in any other insurance market on earth. Founded in 1956 by an act of Parliament, LIC is not merely the largest insurer in India it is the institution through which most of the country experienced insurance for the first time. As of FY 2024–25, LIC commands a market share of 68.58% in terms of new business premiums, an astonishing figure that dwarfs its closest competitor by a factor of more than six.

Between April 2025 and January 2026, LIC collected ₹1,97,887 crore in premiums, representing 57% of industry-wide collections, and posted 14% year-on-year growth. In December 2025, LIC's APE grew 44.1% year-on-year, comfortably outpacing the private sector average of 22.8%.

LIC's claim settlement ratio stands at 96.42%, which, while lower than several private insurers in percentage terms, translates to the highest absolute volume of claims settled — 7,99,612 policies settled within 30 days in FY 2023–24. Its market capitalization stands at approximately ₹5,40,660 crore, making it one of the most valuable financial institutions in India.

From an AI visibility standpoint, LIC is the most mentioned insurance brand across all five platforms tested — unsurprisingly. What is notable, however, is that LIC consistently appears at the top of AI responses even for queries where a private insurer might offer a more technically accurate recommendation. Brand legacy translates directly into AI mindshare.

2. HDFC Life Insurance

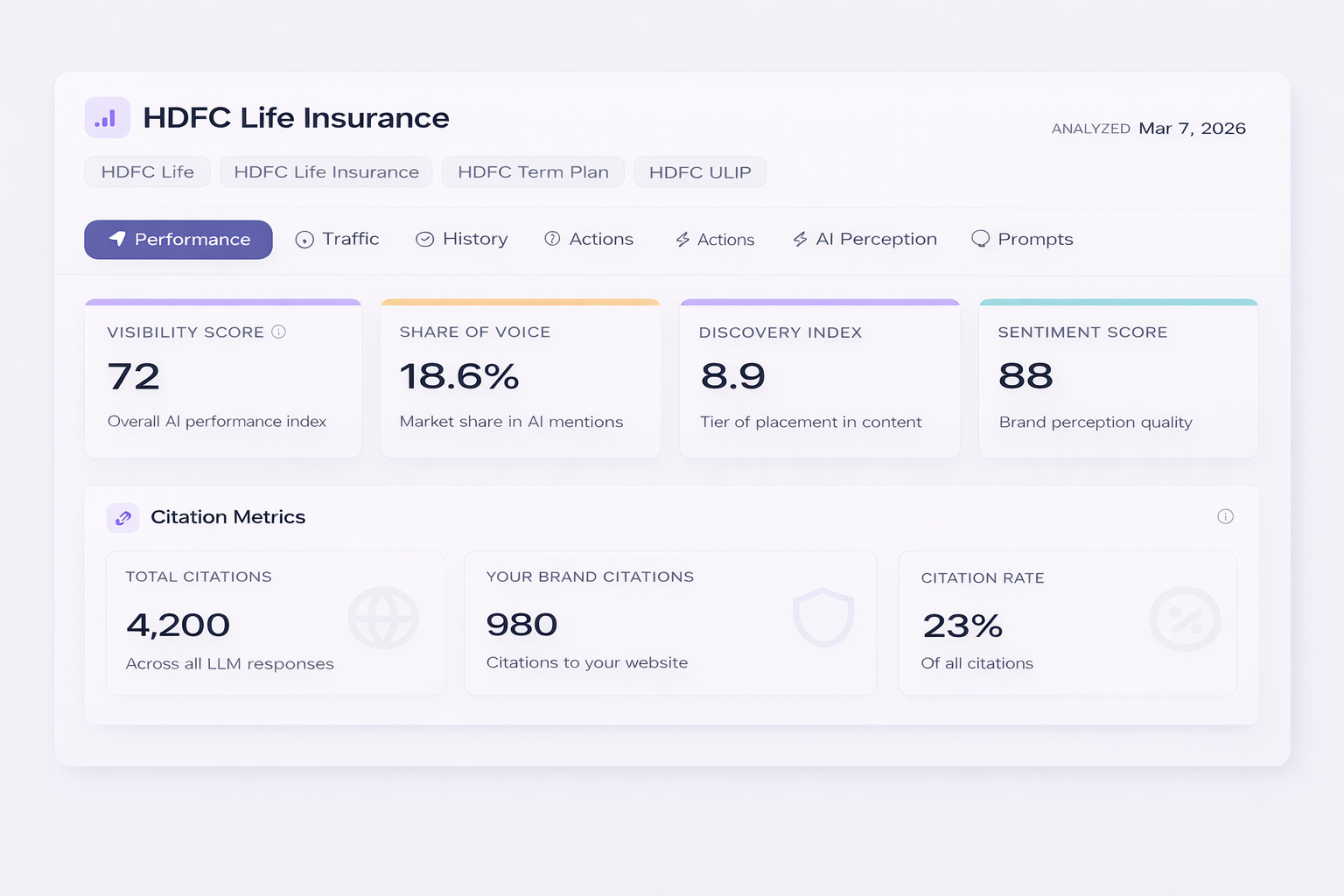

HDFC Life occupies a unique position in India's insurance landscape — it is widely regarded as the most digitally sophisticated among the established large players. Co-promoted by HDFC Ltd and Abrdn, the company holds a 10.22% market share in FY 2024–25 and collected ₹27,904 crore between April 2025 and January 2026, growing 9% year-on-year.

Where HDFC Life truly stands apart is in claims performance. The company achieved a claim settlement ratio of 99.97% in FY 2023–24, settling 19,333 policies within 30 days. In terms of benefit amount paid within 30 days, HDFC Life leads the industry at 99.98% — meaning virtually every rupee of valid claims was paid on time.

HDFC Life's AI visibility profile is strong and consistent. Across comparison queries — particularly those involving premium pricing, digital platforms, and unit-linked insurance plans (ULIPs) — HDFC Life appears frequently as the recommended private insurer. AI models trained on consumer financial content tend to associate HDFC Life with reliability, digital convenience, and transparency.

3. SBI Life Insurance

SBI Life has been one of the standout performers of the past 18 months. Backed by State Bank of India and BNP Paribas Cardif, it currently holds a 10.77% market share in new business premiums — the second highest in the industry. Between April 2025 and January 2026, SBI Life collected ₹34,859 crore in premiums, growing at 18% year-on-year, the fastest growth rate among the top three insurers.

The company's claim settlement ratio of 98.99% — with 37,344 policies settled within 30 days — places it comfortably among the top performers on this metric. SBI Life has also benefitted enormously from its distribution partnership with SBI's 22,000+ branch network, giving it a reach that no purely private insurer can replicate organically.

In IcyPluto's AI visibility analysis, SBI Life consistently appeared in second or third position across most platforms, with AI models frequently highlighting its bancassurance strength and claim settlement performance as key differentiators.

4. ICICI Prudential Life Insurance

ICICI Prudential was one of the first private insurers to enter the Indian market, receiving its licence in 2000 as a joint venture between ICICI Bank and the UK's Prudential PLC. It currently holds a 6.83% market share by new business premiums and remains one of the most recognised insurance brands in urban India.

The company's claim settlement ratio reached 99.3% in FY 2024–25, with the company claiming the title of industry leader in Q2 FY25 with a 99.04% quarterly settlement rate. In terms of benefit amount, ICICI Prudential paid out ₹1,866.88 crore in FY 2023–24.

ICICI Prudential's AI visibility profile is notably strong in ULIP-related and investment-linked queries. The brand's long association with equity-linked insurance products and its broad digital distribution make it a frequent mention in responses to queries about insurance as a wealth-building instrument. This is an important distinction — the brand has successfully carved out a specific thematic corner within AI-generated insurance recommendations.

5. Bajaj Allianz Life Insurance

Bajaj Allianz Life Insurance is the product of a partnership between Bajaj Finserv and the German insurance giant Allianz SE. With a market share of 3.72% in FY 2024–25, it ranks fifth among Indian life insurers by new business premium volume.

The company's claim settlement ratio of 99.78% — settling 14,662 out of 14,695 policies within 30 days — is one of the best in the industry. Bajaj Allianz has also been an early and consistent innovator in digital insurance distribution, launching multiple fintech-adjacent products targeting millennials and gig workers.

In IcyPluto's prompt testing, Bajaj Allianz appeared consistently in responses to queries involving term insurance and online policy purchase — suggesting strong brand-product association for digital-first consumers. The Allianz brand parentage also improves its AI visibility on queries where global credibility is a factor.

6. Tata AIA Life Insurance

Tata AIA Life Insurance operates as a joint venture between Tata Sons and AIA Group, one of Asia's largest pan-regional life insurance companies. It commands a 3.12% market share by new business premiums in FY 2024–25.

The company's claim settlement data reveals a strong operational track record — Tata AIA paid out ₹1,086.15 crore in claims in FY 2023–24, with 99.38% of that amount settled within 30 days. The dual brand heritage — the trust equity of the Tata name in India, combined with AIA's Asian insurance expertise — gives Tata AIA a distinctive positioning that resonates particularly well in tier-1 cities.

Across IcyPluto's AI prompt testing, Tata AIA appeared most frequently in responses involving term life and critical illness covers. The Tata brand's deeply embedded trust in the Indian consumer psyche translates into high AI visibility, particularly for queries about reliable long-term insurance.

7. Kotak Mahindra Life Insurance

Kotak Mahindra Life Insurance, a subsidiary of Kotak Mahindra Bank, currently holds a 2.49% market share in new business premiums. While that figure places it in the lower half of the top ten, the company's growth trajectory and digital infrastructure make it a brand to watch closely.

Kotak Life has distinguished itself through its aggressive digital-first product strategy and its tight integration with Kotak Mahindra Bank's wealth management ecosystem. This positions it well for the next wave of insurance uptake, which is expected to come largely from digitally-enabled middle-class households.

In AI-generated responses, Kotak Life tends to appear in queries related to online term plans and NRI insurance products. Its brand association with the broader Kotak financial ecosystem gives it strong auxiliary visibility in queries that are not explicitly insurance-focused but touch adjacent financial planning topics.

8. Aditya Birla Sun Life Insurance

Aditya Birla Sun Life Insurance (ABSLI) is a joint venture between the Aditya Birla Group and Sun Life Financial Inc. of Canada. With a 3.09% market share in FY 2024–25, ABSLI occupies the eighth position in the industry by premium volume.

ABSLI has built a strong reputation around its ULIP and annuity product portfolio, catering largely to middle and upper-middle income urban professionals. The company has also been proactive in expanding its digital touchpoints, including a direct-to-consumer web platform that allows policy purchase and management without agent intermediation.

In IcyPluto's AI visibility analysis, ABSLI appeared consistently in responses to queries about retirement planning, pension products, and wealth-linked insurance. The Aditya Birla brand's association with diversified, trusted Indian conglomerates lends the insurer credibility across AI-generated financial advice contexts.

9. Axis Max Life Insurance (Max Life Insurance)

Max Life Insurance, now rebranded as Axis Max Life Insurance following Axis Bank's stake acquisition, is arguably the most interesting story in India's private insurance market. With a market share of 3.68% in FY 2024–25, it sits sixth by premium volume but consistently ranks at or near the top for customer service and claims performance.

In the April–January FY26 period, Axis Max Life posted an impressive 20% APE growth, outperforming most of its private-sector peers. Its claim settlement ratio of 99.79% places it as the second-best performer behind HDFC Life. In terms of benefit amount settled within 30 days, Axis Max Life's 99.97% ratio is essentially on par with HDFC Life.

Across IcyPluto's AI testing, Axis Max Life / Max Life appears frequently in responses to queries about best term insurance plans, best claim settlement ratios, and best insurance for young salaried professionals — a trifecta of high-value consumer query categories. The brand's AI visibility significantly exceeds what its market share alone would predict, suggesting strong organic brand equity built through years of consistent customer experience delivery.

10. PNB MetLife India Insurance

PNB MetLife India Insurance rounds out the top ten, with a 1.42% market share in FY 2024–25. The company operates as a joint venture between Punjab National Bank and MetLife International, and its distribution is anchored by PNB's extensive semi-urban and rural branch network.

PNB MetLife's positioning is distinctly different from its peers — rather than competing head-on in the digital-native or urban affluent segment, it focuses on accessible protection products for first-time insurance buyers in tier-2 and tier-3 markets. This approach has given it consistent, if modest, premium growth.

In AI-generated responses, PNB MetLife tends to appear on lists of recommended insurers for price-sensitive buyers, rural-market focused products, and government-linked insurance schemes. Its visibility in AI tools is driven by regulatory mentions and comparison lists, rather than the thematic product associations that drive visibility for brands like ICICI Prudential or Kotak Life.

IcyPluto's analysis of 10,000+ prompts across five LLM platforms produces a clear hierarchy of AI brand visibility and it does not perfectly mirror the traditional market share rankings. This is one of the most important findings of this report.

The AI Visibility Rankings

Based on frequency of appearance, position within AI responses, and cross-platform consistency, here is how the top 10 insurers rank on AI brand visibility:

Tier 1 Dominant AI Presence (appears in top 3 on virtually all platforms):

LIC: Unrivalled. Appears first or second in nearly every insurance-related query across all five platforms.

HDFC Life: The strongest private-sector AI brand. Consistently appears when queries involve quality, reliability, or claims.

SBI Life: Strong across general and government-related queries. Banks on its SBI parentage for broad query coverage.

Tier 2 Strong AI Presence (appears consistently, often in top 5):

ICICI Prudential: Dominates ULIP and investment-linked insurance query categories.

Axis Max Life: Punches well above its market share rank — strongest AI visibility-to-market-share ratio in the private sector.

Bajaj Allianz: Strong in term insurance and digital purchase queries.

Tata AIA: Strong in trust-heavy and critical illness queries.

Tier 3 Moderate AI Presence (appears frequently but not universally):

Aditya Birla Sun Life: Visible in retirement and pension-related queries.

Kotak Life: Visible in digital, NRI, and wealth management queries.

PNB MetLife: Appears primarily in comprehensive lists and rural/government-linked insurance contexts

Perhaps the most actionable insight from IcyPluto's research is the divergence between traditional market share and AI brand visibility. LIC's dominance in both dimensions is expected and self-reinforcing. But among private insurers, the gap is significant.

Axis Max Life, despite ranking sixth by market share, consistently appeared in the top three or four positions in AI responses — often beating ICICI Prudential and Bajaj Allianz on comparative queries. This suggests that Axis Max Life's superior claims performance and customer satisfaction scores have been indexed deeply into the training data of these AI models, resulting in a brand visibility premium that purely financial metrics do not capture.

Conversely, PNB MetLife and Kotak Life despite being well-capitalised, established brands — show relatively lower AI visibility outside of niche query categories. For marketing strategists at these companies, this is a clear signal: if AI-generated search responses increasingly drive consumer discovery, their brand presence in this channel needs active investment and measurement. This is precisely the kind of insight that IcyPluto's GEO infrastructure is designed to surface and act upon.

Five Trends Defining India's Insurance Market Through 2026 and Beyond

The competitive dynamics in India's insurance sector are not static. Several structural trends are reshaping the industry in ways that will determine the winners and losers of the next decade.

Digital Distribution Is No Longer Optional

India's online insurance segment is the fastest-growing channel in the market. The pandemic permanently shifted a significant portion of policy purchases and renewals online, and that shift has proved durable. Insurers that have invested heavily in direct-to-consumer digital platforms — HDFC Life, Bajaj Allianz, and ICICI Prudential most prominently — are reaping the rewards through lower distribution costs and faster customer acquisition cycles.

The government's Bima Sugam initiative, a centralised digital marketplace for insurance products, is set to further accelerate this shift. Bima Sugam will allow consumers to compare, purchase, and manage insurance policies across providers through a single digital platform — fundamentally disrupting the traditional agent-led distribution model that companies like LIC have historically relied upon.

The GST Waiver Has Changed the Premium Maths

The GST waiver on individual life and health insurance premiums introduced in 2025 has had a measurable impact on policy uptake. By removing an 18% tax layer from premium payments, the waiver effectively reduced the out-of-pocket cost of life insurance for millions of Indian households — particularly in the recurring premium product segment. CareEdge Ratings has cited the GST waiver as one of the primary drivers of the December 2025 premium surge.

This policy change is likely to sustain above-average growth in individual new business premiums well into FY 2026–27, especially in tier-2 and tier-3 markets where price sensitivity is the primary barrier to insurance adoption.

AI and Predictive Analytics Are Redefining Underwriting

The use of AI in insurance underwriting, fraud detection, and customer lifetime value modelling is accelerating across India's top insurers. Both HDFC Life and ICICI Prudential have made public commitments to embedding AI into their core operations. Tata AIA has leveraged AIA Group's regional AI capabilities to improve risk pricing across its product portfolio.

This matters for a brand visibility perspective too. As consumers increasingly interact with AI tools to research insurance options, the brands that are most accurately and positively represented in AI training data will have a structural advantage in the next generation of customer acquisition. This is the central thesis behind IcyPluto's GEO work and it is becoming increasingly relevant to every major financial services brand in India.

Claim Settlement Performance Is Now a Marketing Asset

The emergence of IRDAI's annual claims data as a widely-discussed consumer reference point has changed the competitive dynamics in Indian insurance marketing. A decade ago, claim settlement ratios were footnotes in actuary reports. Today, they are headline metrics in consumer comparison platforms, social media content, and — as IcyPluto's research confirms — AI-generated recommendations.

HDFC Life's 99.97% and Axis Max Life's 99.79% claim settlement ratios are not just operational achievements — they are marketing assets that actively improve these brands' AI visibility scores across comparison and trust-signal queries. For insurers further down the claims performance table, closing this gap is not just an operational priority; it is a brand strategy imperative.

India's Insurance Penetration Story Is Only Getting Started

India's insurance penetration — at roughly 3.2% of GDP — remains well below the global average of around 7%. The macro story is straightforward: as India's per capita income rises, urbanisation deepens, and financial literacy improves, the addressable market for life insurance will expand dramatically.

Swiss Re's projection of 6.9% annual real growth from 2026 to 2030 is built on this foundation. For the companies in this report, that growth will not be distributed equally. The brands that invest in digital distribution, AI-powered customer engagement, and GEO-driven brand visibility will capture a disproportionate share of the next wave of first-time insurance buyers. This is a market where brand intelligence — real-time, AI-driven, cross-platform brand intelligence — will be the decisive competitive variable.

India's insurance sector is more competitive than at any point in its post-liberalisation history. Ten brands dominate the conversation — in boardrooms, in distribution networks, in regulatory filings, and increasingly, in the responses generated by AI tools that millions of Indians now use to make financial decisions.

IcyPluto's analysis of 1,000+ prompts across five leading LLMs reveals that AI brand visibility is a measurable, actionable dimension of competitive positioning — one that does not always correlate with market share or advertising spend. Brands like Axis Max Life and HDFC Life have earned high AI visibility through operational excellence and consistent consumer trust signals. Brands with lower AI visibility, despite strong fundamentals, are leaving discovery opportunities on the table.

For brand and marketing leaders in India's insurance sector, the message is direct: the next battleground for market share is not just the offline agent network or the digital ad auction. It is the training data, the associative memory, and the response logic of the large language models that your potential customers are already consulting. Winning that battle requires a new kind of intelligence infrastructure — and that is exactly what IcyPluto is built to provide.